Meet Our Residential Underwriting and Legal Team

As an industry leader and authority on the local real estate market, you can count on Republic Title’s highly trained teams and in-house attorneys to ensure your transaction closes quickly, with fast turnaround on title searches and underwriting decisions. We are proud to highlight our Residential Underwriting and Legal team who are available to answer […]

Republic Title Mobile

If you haven’t downloaded our app, Republic Title Mobile, now is the time! Join other real estate agents using Republic Title Mobile and see why we have a 5 star rating in the Apple Store! Republic Title Mobile is a mobile app that provides easy access for real estate professionals, buyers, and sellers to closing […]

The ABC’s of Title Commitment

A commitment is a document the title company provides to all parties connected with a particular real estate transaction. It discloses the title of record to the property as well as liens, defects, burdens and obligations that affect the subject properties. It is comprised of four schedules. Schedules A, B, C, and D are as […]

What To Expect At Closing

https://youtu.be/XnVBLy9lhC4 There are many steps in the home buying process – saving, searching, shopping, inspecting, etc. Once you get through all of these steps, you have finally made it to the closing table and are so close to being in your new home! Here’s a brief description of what to expect at closing: The Buyer […]

Spanish Resources

Republic Title offers multiple real estate resources in Spanish for home buyers and sellers including: The Closing Process / el Proceso de Venta Republic Title – Who we are and why you need Title Insurance / Republic Title – Quienes somos y porque necesita una compania de titulus Republic Title Locations / Ubicaciones de Republic […]

Home Seller’s Guide

Home Seller’s Guide Digital Flipbook – Republic Title We are excited to introduce our new Home Seller’s Guide that is available as a luxury printed booklet or as a digital download. Our Home Seller’s Guides have everything that you need to know for a smooth home selling process. Our Home Seller’s Guide includes information on: […]

Closing Process Overview

We are continuing to celebrate National Homeownership Month which is a time to celebrate the benefits that homeownership brings to families and communities. In honor of National Homeownership Month, we have curated a list of our most popular homeownership resources for new homebuyers. Next up is our Closing Process Overview. When you are preparing to […]

Lingo You Should Know When Buying a Home

We are continuing to celebrate National Homeownership Month which is a time to celebrate the benefits that homeownership brings to families and communities. In honor of National Homeownership Month, we have curated a list of our most popular homeownership resources for new homebuyers. Next up is our Lingo You Should Know. When you are preparing […]

Home Buying Road Map

We are continuing to celebrate National Homeownership Month which is a time to celebrate the benefits that homeownership brings to families and communities. In honor of National Homeownership Month, we have curated a list of our most popular homeownership resources for new homebuyers. Next up is our Home Buying Road Map. Buying a home is […]

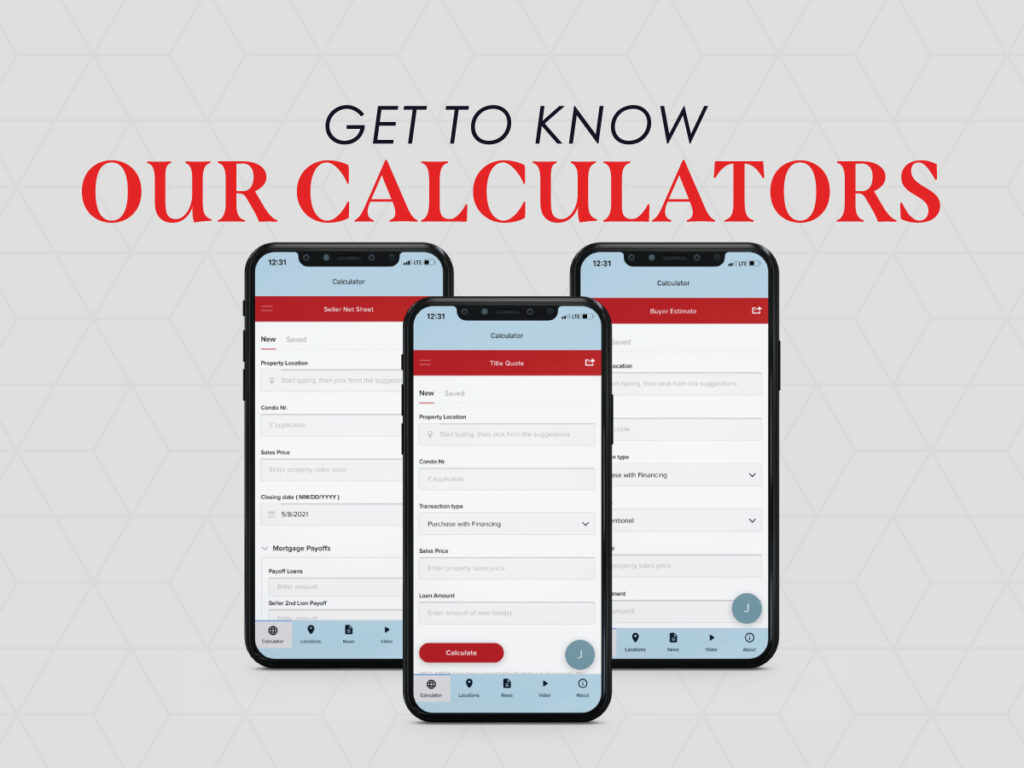

Get To Know Our Calculators

Republic Title is proud to offer a host of new buyer and seller estimate tools on our Republic Title Mobile app and website. Calculators include: Title Quote – calculates title rates and fees Loan Estimate Quote – shows the costs associated with closing on your mortgage as well as over the lifetime of the loan Seller Net Sheet […]