Get To Know Our Calculators

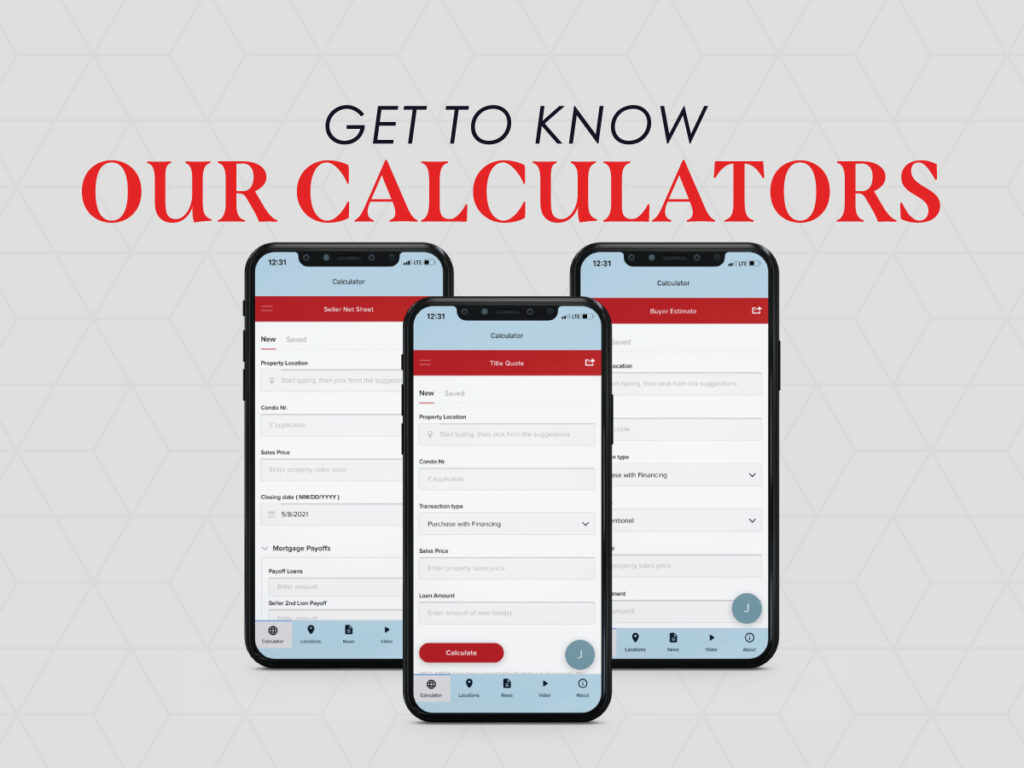

Republic Title is proud to offer a host of new buyer and seller estimate tools on our Republic Title Mobile app and website. Calculators include:

Republic Title is proud to offer a host of new buyer and seller estimate tools on our Republic Title Mobile app and website. Calculators include:

https://youtu.be/2p75rKEChXM The March 2021 DFW area real estate statistics are in and we’ve got the numbers! Our stats infographics include a year over year comparison and

Total Texas housing sales plummeted 16.1 percent in February as Winter Storm Uri swept across the state, causing widespread power and water outages. Before the